|

|

|

|

|

Forecasting Functions

Forecasting functions use additional parameter Length, referred in the following descriptions as 'n' or 'a'.

Moving Average

Unweighted mean of the previous 'n' data points.

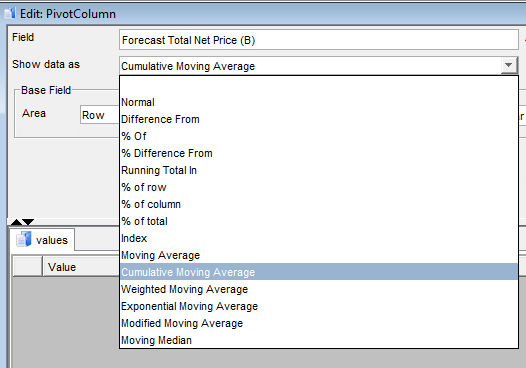

Cumulative Average

Average of all of the data up until the current data point.

Weighted Average

A weighted moving average (WMA) has weights that decrease in arithmetical progression. In an n-day WMA the latest day has weight n, the second latest n - 1, etc., down to one.

Exponential Moving Average

An exponential moving average (EMA), also known as an exponentially weighted moving average (EWMA), is a type of infinite impulse response filter that applies weighting factors which decrease exponentially. Weighting for each older data point decreases exponentially, never reaching zero.

Parameter Length defines 'a' in the following formula:

![]()

If specified Length > 1 ,then a = 1/Length, because 'a' must be in the interval (0, 1).

Modified Moving Average

A modified moving average (MMA), running moving average (RMA), or smoothed moving average is defined as:

![]()

In short, this is exponential moving average, with a = 1 / N.

Moving Median

From a statistical point of view, the moving average, when used to estimate the underlying trend in a time series, is susceptible to rare events such as rapid shocks or other anomalies. A more robust estimate of the trend is the simple moving median over 'n' time points:

![]()

Depending on the selected modification function there should be specified Base Field and in some cases Base Item. Base Field and Base Item serve as reference data for the calculation.

Example:

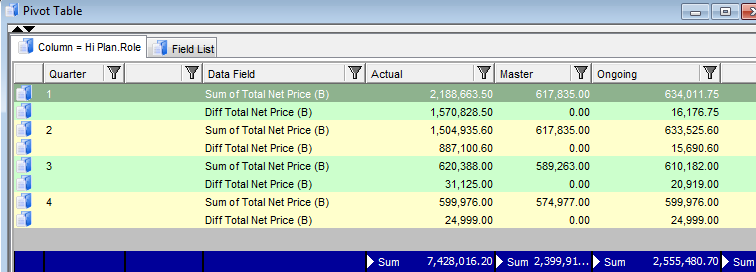

Let’s calculate difference of expenses in each plan to the expanses in Master plan.

- Switch to the Field List

- Select "Total Net Price (B)" and run action Copy

- New field is created with name “Total Net Price (B)1” and opened in the editor

- Change the name to “Diff Total Net Price (B)”

- In the Show data as select “Difference From”

- In the Base Field select “Hi Plan.Role"

- In the Base Item select “Master”

- Press 'OK'

- Switch to the results reference catalog and press button 'Refresh'

In this case the field from column area is used as a Base Field. The same behaviour can be achieved for column and page areas.

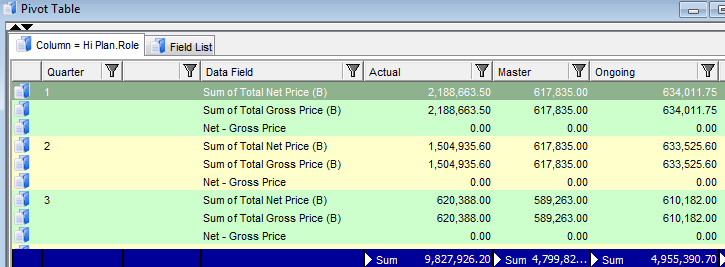

Another example would be if we want to show difference between two values in the data area.

Let’s calculate difference of Total Net Price and Total Gross Price.

- Switch to Field List

- Select fields Total Net Price (B) and Total Gross Price (B) and press button [Data Area]

- Select “Total Net Price (B)” and run action Copy

- New field is created with name “Total Net Price (B)1” and opened in the editor

- Change the name to “Net – Gross Price (B)”

- In the Show data as select “Difference From”

- In the Base Field select “Total Gross Price”

- In the Base Item select “Master”

- Press 'OK'

- Switch to the results reference catalog and press button 'Refresh'